According to a study jointly conducted by LIMRA and Boston Consulting Group (BCG), Change Management has become the most important challenge in the minds of C-suite executives in the global life insurance industry, followed closely by the need to improve customer experience. Results from the new biennial global survey of C-suite life insurance executives finds a shift in priorities as economic, technological, regulatory and consumer changes press life insurance companies to reassess their business model.

Read Also: Voicify Conversation Experience Platform™ Powers Vodka Company to Drive Meaningful Chats

The study surveyed more than 500 C-suite life insurance executives, nearly one-fifth of them CEOs or presidents, across 62 countries to identify their greatest challenges and the biggest external forces affecting their business and their priorities for the future. The findings are presented in a report titled “What’s On the Minds of Life Insurance Executives: Managing Change in a Customer-Focused World.”

Change Management Closely Ties into the Customer Experience Efforts

Change management emerges the greatest internal challenge facing life insurance executives as they work to help their organizations keep pace with and adapt to a rapidly evolving business environment. The study finds one-third of executives cite change management as their greatest challenge. This is a significant shift from prior studies in 2015 and 2017, when executives cited talent management as their biggest challenge.

Read More: Companies Using AI and IoT Together Catapult Ahead of Competitors Using IoT Alone

“In today’s business environment, executives are realizing that having the right talent is not enough to address the external forces transforming the business landscape,” said Alison Salka, Ph.D., senior vice president and director of LIMRA Research.

Alison added, “To transform their entire organizations, executives must cultivate corporate cultures that not only fully embrace change, but can also sustain it over the long term.”

Part of this need to better manage the change in their organization is the recognition that life insurance companies need to improve their customer experience. Nearly a quarter of executives said this was a top challenge for their company. As leading companies embrace advanced IT and data capabilities to analyze customer behavior, cross-sell and customize products, other companies appreciate the need to invest in these technologies to compete for consumers’ attention.

“Life insurance executives have long been aware they need to change their organizations and deploy new digital technologies to improve customer experience, become more efficient, and develop products that are more tailored to individual needs,” said Tim Calvert, managing director and partner and global leader of BCG’s Life Insurance practice.

Tim added, “Our research indicates that they are now ready to do something about it.”

External Challenges Driving Change

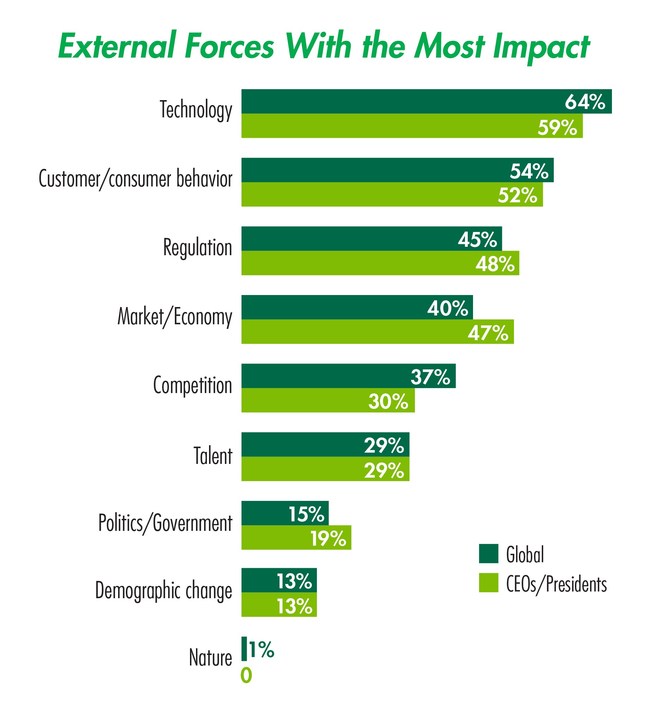

As life insurers look to transform, there are external factors that are also spurring change. Nearly two-thirds (64%) of executives surveyed said technology such as artificial intelligence, automation, and customer-service tools, would have the greatest impact on their company in the next five years, followed by customer behavior and regulations (Chart 2).

“Advances in technology offer the most promise to help insurers transform their business but also reveal the acute talent management challenges they face,” noted Calvert. “IBM reports the competition for skilled data scientists will increase nearly 30% by 20201. Insurers are grappling with not only finding qualified candidates but retaining these individuals in a highly competitive marketplace.”

Regulation also plays a significant role in driving change. The strong push in many countries for greater fiduciary and suitability standards; transparency over pricing, commissions, incentives; and consumer privacy protection means that the regulatory environment will continue to have important implications for life insurers.

When asked to name the most challenging areas for regulation and compliance, “customer best interest,” cited by 47% of executives worldwide, was the leading issue. This was closely followed by “analytics/modeling in risk compliance,” “data privacy,” and “cyber security.”

“Fraud is also a growing concern among life insurance executives. More than three-quarters of CEOs and executives overall worry about the growing incidence of fraud,” Salka remarked. “Fraud not only hurts a company’s bottom line but damages its reputation and consumer trust. This concern led LIMRA to develop FraudShare, a new tool to help insurers better detect and prevent account takeover attempts.”

The report’s authors offer three suggestions for life insurers to consider as they realign, reimagine, and transform their companies for tomorrow:

Instill a pro-change culture. A corporate culture of change is a pre-requisite if life insurers are to make their businesses more customer-centric. That begins with having the right people across the organization that believe in change.

Focus on the customer. The first thing to remember about improving the customer experience is that authenticity and agility are key. Insurers need to better understand the needs of their customers by closely and regularly monitoring customer journeys to determine what is going well and what needs to improve.

Think strategically about technology. For the industry to truly achieve the quality of digital experience and operational efficiency they desire, technology must become more central to the overall business strategy and be viewed as a source of competitive advantage—rather than merely a cost.

Serving the industry since 1916, LIMRA helps to advance the financial services industry by empowering nearly 600 financial services companies in 64 countries with knowledge, insights, connections and solutions.

, Change Management has become the most important challenge in the minds of C-suite executives.){kind=link}