For businesses focused on retention within the customer lifecycle, a key question is how to tell when your customers are thinking of leaving? While this question can be applied across a range of industry verticals, it is very apparent in the competitive fuel industry, where a customer may hold multiple fuel cards from different providers. Ensuring a card is consistently used by remaining ‘front of wallet’ is, therefore, a key priority.

For businesses focused on retention within the customer lifecycle, a key question is how to tell when your customers are thinking of leaving? While this question can be applied across a range of industry verticals, it is very apparent in the competitive fuel industry, where a customer may hold multiple fuel cards from different providers. Ensuring a card is consistently used by remaining ‘front of wallet’ is, therefore, a key priority.

Sometimes there are obvious signs that a customer is about to leave, such as declining purchase volumes; but conversely, some customers leave with no warning at all. However, when a fuel card issuer has hundreds, if not thousands of customers, it is impractical to conduct a manual in-depth analysis of each one to try and answer this question. Not to mention that by the time that sort of analysis has been concluded, the customer may have already left.

Machine Learning (ML) models are consequently a more convenient and efficient way of trying to predict ‘customer churn’. As well as offering faster processing times, these algorithms can also pick up underlying behavioral patterns that are not visible to the human eye. Using the latest ML technology, it is now possible to create customer churn algorithms based on historical data; which, when applied to real-time data, can help predict which customers pose a churn risk.

How this works in practice

Having access to a large set of historical data is a key aspect of this work; as it not only builds the customer profiles and the corresponding churn model but allows a sizeable portion of data to be set aside for validation and testing. By looking at all customers that have churned (based on a halt in their purchasing activity) within a training data set, common patterns can be established in the behavior of these customers leading up to them leaving.

That model can then be used on the ‘validation’ data to see if any churners can be accurately predicted. Optimization can be conducted by modifying variables in the model, iteratively retraining on the training data and validating on the validation data, until an optimal model for prediction is created. This optimized model is finally applied to the previously unseen test data so that when it comes to analyzing unseen, real-time behavioral trends, there can be a high degree of confidence in accurate churn prediction.

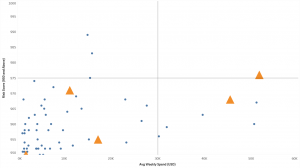

By scoring customers between 0 and 1000 for the likelihood of ‘churning’, we can segment customers in terms of average weekly spend to create a risk versus value matrix:

|

High Risk, Low Value |

High Risk, High Value |

|

Low Risk, Low Value |

Low Risk, High Value |

(Fig 1.)

In doing so, we have created a visualization guide, which allows a fuel card issuer to take a more focused approach on specific customers to target for retention (i.e. high risk, high-value customers). Even though the below visualization guide indicates that not all customers who were in the right (high value) half of the risk matrix churned, this model suggests it could potentially save 2 in 7 of the highest risk, high spend customers (a potential 29% increase in retention).

(Fig 2.)

(Fig 2.)

If we extend the retention campaign to focus on the top 20 highest value customers, 20% of customers would have been accurately predicted as churners. Within this example, this equated to a possible retention value of ~$125K per week had remediation steps have been taken, a total of $6.5 million in annual revenue.

It is also important to note that high-risk customers who did not churn at the time of this visual being created, could still go on to churn later. So, although contacting customers that ‘wouldn’t have left anyway’ might seem like a waste of effort, this methodology also delivers the benefit of keeping high-value customers engaged. Potentially reducing their risk score over the longer term, so that they are less likely to churn in the future.

Of course, there is no guarantee of ensuring a fuel card customer stays even after a targeted approach, but by identifying the potential risk before a churn event, it allows fuel card issuers to take measures on ensuring customer loyalty. This can be through offers, such as specific promotions and discounts, or simply having a discussion with the customer on what fuel card options they would like to have available to them.

Readers who are familiar with the film ‘Minority Report’ may be familiar with the film’s concept of psychic ‘precogs’ predicting crimes before they occur. Much like the film’s crimes (spoiler alert), we can never be 100% sure that a churn event will happen unless we let it happen.

While this presents some ambiguity in measuring success, we can anticipate around 10-30% increased retention. This can be calculated using an average of prior year retention rates, compared to retention after the model and visualization have been in use for some time.

The time to act

Another model output to consider is the ‘time to act window’. In an ideal scenario, both prediction accuracy is high, and the length of time before a churn event that a prediction can be made is long enough for a card issuer to reach out to the at-risk customer.

In the example illustrated in Fig 2. above, the optimal model window is a month. However, based on available data and ensuring a significant accuracy in churn prediction, another model created for a different business could have a much shorter window.

From a practical standpoint, this might not give a card issuers enough time to take steps for reaching out to their customers and trying to retain them. While there is not necessarily a trade-off between prediction accuracy and time to act; understanding how fast a business is willing to react plays an important role in making sure a model meets the needs of the fuel card issuer.

The dawning reality is that incorporating ML as a tool is now an essential part of customer lifecycle management. Fuel card issuers without it are not only at risk of losing customers to better- equipped competitors, but high-value customers may stay away due to the improved retention methods of leaders using this technology. Therefore, the biggest indicator of success is that your business is already at least exploring how this technology can be applied, as, without it, you may be left behind by your customers leaving you.

Read more: How Marketing Can Help Develop an Effective Customer Onboarding Program

{kind=link}